Itô process is like a generalized random walk and Itô’s lemma gives us a formula for doing calculus with Itô processes.

Itô Process

An Itô process is defined as a stochastic process of the form

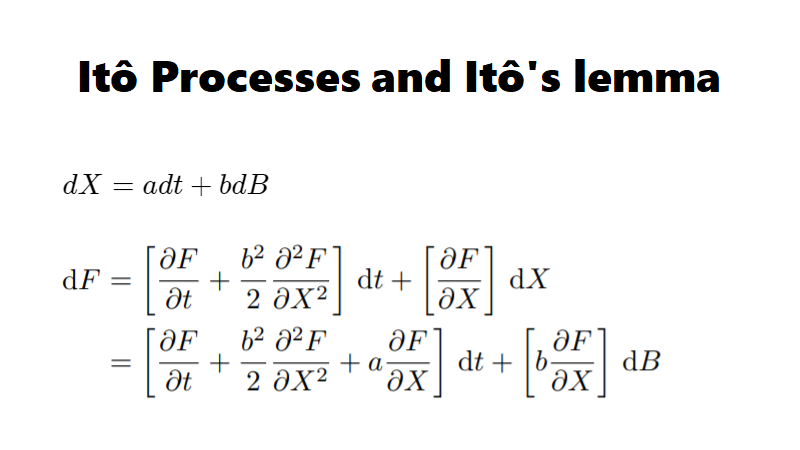

dX = adt + bdB

where X and B are both time dependent and B is a Guassian Brownian random variable.

adt is a deterministic component of the Ito process, while bdB is stochastic.

Deterministic means you can calculate a future event exactly, without the involvement of randomness. If something is deterministic, you have all of the data necessary to predict (determine) the outcome with certainty.

Stochastic, on the other hand, involves some inherent randomness. The same set of parameter values and initial conditions will lead to an ensemble of different outputs.

A Brownian path is continuous everywhere, differentiable nowhere. Therefore, B and X are not differentiable.

If F is a function of X, how do we differentiate F? We use Itô’s lemma (aka Itô’s Formula).

Itô’s Lemma

\begin{aligned}

dF &= \left[\frac{\partial F}{\partial t} + \frac{b^2}{2}\frac{\partial^2 F}{\partial X^2} \right]dt + \left[ \frac{\partial F}{\partial X}\right]dX\\

&= \left[\frac{\partial F}{\partial t} + \frac{b^2}{2}\frac{\partial^2 F}{\partial X^2} + a\frac{\partial F}{\partial X} \right]dt + \left[b\frac{\partial F}{\partial X} \right]dB

\end{aligned}This formula denotes that dF is itself an Itô process as it consists of a deterministic term (dt) and a stochastic term (dB).

You can view the formula as the usual chain rule for partial differentiation, plus an extra term:

dF = \frac{\partial F}{\partial t} dt + \frac{\partial F}{\partial X} dX + \frac{b^2}{2}\frac{\partial^2 F}{\partial X^2} dtExamples

Geometric Brownian motion with drift

Geometric Brownian motion with drift is modelled by the equation

dS = \mu Sdt + \sigma S dB

We can rewrite dS as

\begin{aligned}

dS &= adt + bdB, \quad where\; a = \mu S, b = \sigma S\\

\frac{dS}{S} &= \mu dt + \sigma dB

\end{aligned}dS/S is not integratable (why?). Therefore, we need to use Itô’s lemma

\begin{aligned}

\text{Let }F &= log(S)\\

\frac{\partial F}{\partial t} &= 0\\

\frac{\partial F}{\partial S} &= \frac{1}{S}\\

\frac{\partial^2F}{\partial S^2} &= -\frac{1}{S^2}\\

\end{aligned}Applying Itô’s lemma,

\begin{aligned}

dF &= d(log S)\\

&= \frac{1}{S}dS + \frac{(\sigma S)^2}{2}\left(\frac{-1}{S^2}\right)dt\\

&= \mu dt + \sigma dB - \frac{\sigma^2}{2}dt

\end{aligned}Therefore,

d(logS) = \left( \mu - \frac{\sigma^2}{2} \right) dt + \sigma dBIntegrating on both sides from 0 to T,

\begin{aligned}

log\left(\frac{S_T}{S_0} \right) &= \left(\mu - \frac{\sigma^2}{2} \right)T + \sigma(B_T - B_0)\\

S_T &= S_0^{\left(\mu - \frac{\sigma^2}{2} \right)T + \sigma(B_T - B_0)}

\end{aligned}

Leave a Reply