In this post, we’ll learn to convert a AR(1) model to a MA model.

The moving-average model specifies that the output variable depends linearly on the current and various past values of a stochastic (imperfectly predictable) term.

https://en.wikipedia.org/wiki/Moving-average_model

So, a MA model should only depend on zt-k, where k >= 0.

Converting a AR(1) Model to a MA model

Rt – μ = -λ(Rt-1 – μ) + σ*zt —————– (1)

Let

yt = (Rt – μ)/σ

Dividing (1) by σ,

(Rt – μ)/σ = -λ(Rt-1 – μ)/σ + zt

yt = -λyt-1 + zt

Similarly,

yt-1 = -λyt-2 + zt-1

yt-2 = -λyt-3 + zt-2

etc

Therefore,

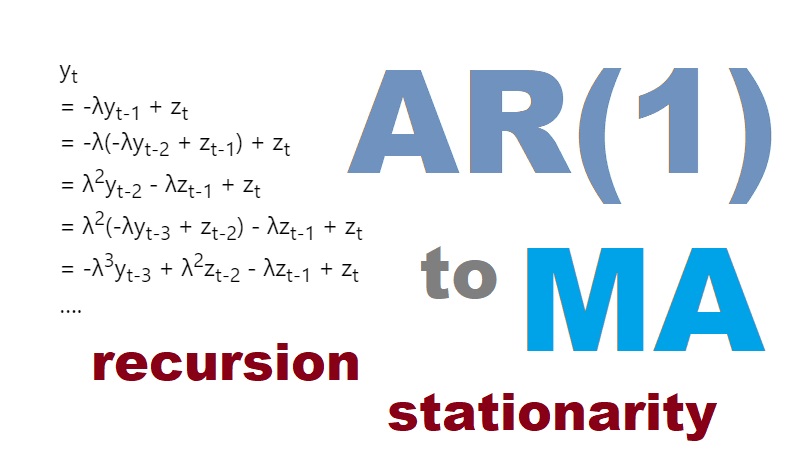

yt

= -λyt-1 + zt

= -λ(-λyt-2 + zt-1) + zt

= λ2yt-2 – λzt-1 + zt

= λ2(-λyt-3 + zt-2) – λzt-1 + zt

= -λ3yt-3 + λ2zt-2 – λzt-1 + zt

….

Since λ is the multiplier for Rt−1, it should be smaller than one as the effect of Rt−1 dies off over time.

Therefore, as we keep replacing yt-k, the y-term eventually gets multiplied by a very small value of λk and becomes insignificant.

Therefore,

yt = sum of (-λ)kzt-k for k from 0 to infinity

Since

yt = (Rt – μ)/σ

Rt = σyt + μ

Since yt only depends on values of zt-k, Rt only depends on zt-k too, where k>=0.

In other words, Rt only depends on current and past values of z. We have successfully converted it to a MA model.

Useful conclusion:

E[zsyt] = 0 for t < s

This means zs and yt are independent. Put it another way, yt does not depend on zs, where s is a future time compared to t. Therefore,

E[zt(Rt-1 – μ)] = 0

which is an intuitive property that we stated when solving the AR(1) model previously.

Leave a Reply